How to speed up your accounting closing? Everything you need to know

Publié

Le 21/04/2022, par :

- Anne Marie Diom

Sections

Contexte

Companies are faced with a large number of manual tasks that often lead to data entry errors when closing the financial year. Some companies still spend a majority of their time manually making lists, reconciliations and audit trails.

However, errors can cost them dearly. CALIXYS gives you all the information you need to better prepare for closing the financial year.

But what is accounting closure?

Closing the accounting year is a mandatory process that companies must perform every year on the same date. It is not mandatory for people carrying out an activity under the simplified tax regime and micro-enterprises.

This process allows you to edit and adjust account balances in order to assess the financial health of the company. If you are a manager, this accounting exercise will allow you to analyze the relevance of the strategies implemented.

However, you cannot start next year’s accounting year if you have not submitted your annual accounts for the previous year.

For this process, you must record all your entries for the year in question and have all the transactions and supporting documents in order to modify your company’s report.

The 3 documents required to carry out this exercise

The income statement presents all recorded expenses and income. It groups together all gains and losses over the accounting year. It can be divided into 3 subcategories: operating, financial and exceptional.

The income statement

To complete and file your accounting exercise, you must have a series of documents in order to comply with certain rules and criteria. These documents will allow you to justify your balance sheet, but also to check, complete and correct your results.

The accounting balance sheet

The balance sheet evaluates the company’s assets in order to determine its financial value and sustainability. It takes the form of a table with 2 columns, the right column representing everything it owes (liabilities) and the left column showing everything it owns (assets).

In the balance sheet, you must follow different steps:

Prepare all the necessary documents that will allow you to modify, complete and justify the balance sheet.

Evaluate and carry out the accounting inventory work.

Carry out the account review work.

The accounting annex

The accounting appendix will provide details on the income statement and the balance sheet. They contain 2 pieces of information: mandatory information and information of significant importance.

The 3 steps to successful accounting closing ?

Before embarking on this accounting exercise, it is necessary to take into account several steps to better understand all the elements in order to establish a clear and effective accounting balance sheet.

This mission involves a significant amount of time and investment.

Entering accounting entries

Once you have all the necessary documents, you must absolutely justify the existence of each accounting entry and check that each line is present in your accounting tool or in your general ledger.

Classify your different accounting entries of the year by categories to facilitate your operations and have a better overview.

It is also necessary to evaluate the state of the stocks, identify the products and the expenses present as well as the cash flow. You must pay attention to duplicates in your entries and avoid tax fraud and data entry errors.

The accounting annex

This review allows you to check the accounting balances before modifying the balance sheet.

To do this, accounts must be checked for the closing of the accounting year. However, we advise you to review your accounts during the year to facilitate the day of this accounting year.

But, which accounts need to be reviewed?

Cash accounts: the balances must be reconciled. They must be compared with their cash statement. All differences must be justified.

Customer and supplier accounts: the balances of a customer account often correspond to unpaid invoices. To avoid unpaid risks, delays and errors, the reconciliations between the customer account balance and the general account balance must be identical. The same operation applies to the control of supplier accounts.

Social and tax accounts: the balances are reconciled with their declarations (VAT and payroll, etc.) and the slips.

The audit of the accounts must be documented for use in the next year’s accounting period and this document also serves to justify the processes in the event of problems.

Save accounts

After checking the accounts and entering the accounting entries, the company must modify, complete and justify its balance sheet and income statement which are, as mentioned above, documents necessary to close the accounting year.

These documents are important to assess the financial health of the company and its performance in terms of losses and profits.

It is essential to have a tool that will allow you to control your accounting operations and have a 360° view of the financial health of your company.

When and who should carry out the accounting closing ?

The actors who can carry out the closing of the accounting year are:

The company manager

He can carry out the accounting balance sheet using accounting tools to analyze his cash flow, data reliability and expenses. However, it is necessary to have expertise in accounting to avoid errors.

The chartered accountant

He will audit company accounts and tax returns.

The accountant

It will record the transactions in accounting, check the tax returns and prepare the balance sheet manually.

But what date should be chosen for the closing of the accounting year?

Generally, the accounting year begins on January 1st and ends on December 31st. However, companies have the possibility to choose the date of their accounting closing. The condition of this choice is that the date is the same for all years. The accounting year must extend over 12 months.

What are the challenges in closing the accounts ?

The accounting year can be complicated, especially if you have several accounts to control and reconcile or if you are present internationally. CALIXYS presents the 3 main challenges related to the closing of the accounting year.

Unreliable or missing data

Duplicates, unrecorded payments, simple data entry errors, unrecorded invoices, inaccurate data, calculation errors, incomplete fields, all these problems generate time in the company.

Human errors

CFOs and accountants are faced with manual and repetitive tasks, making the closing process a challenging task. They also have tight deadlines to meet. All of these factors can lead to errors and fraud.

Des systèmes disparates

Dans les services financiers, il n’est pas toujours facile de trouver rapidement toutes les données. Cela se complique encore plus dans les entreprises qui sont présentes à internationales et qui possèdent différents comptes.

Certaines utilisent des logiciels comptables, mais ils ne sont pas toujours adaptés à leur organisation et leur processus d’intégration peut être long. Tous ces problèmes peuvent réduire l’efficacité du personnel et retarder la clôture de l’exercice comptable.

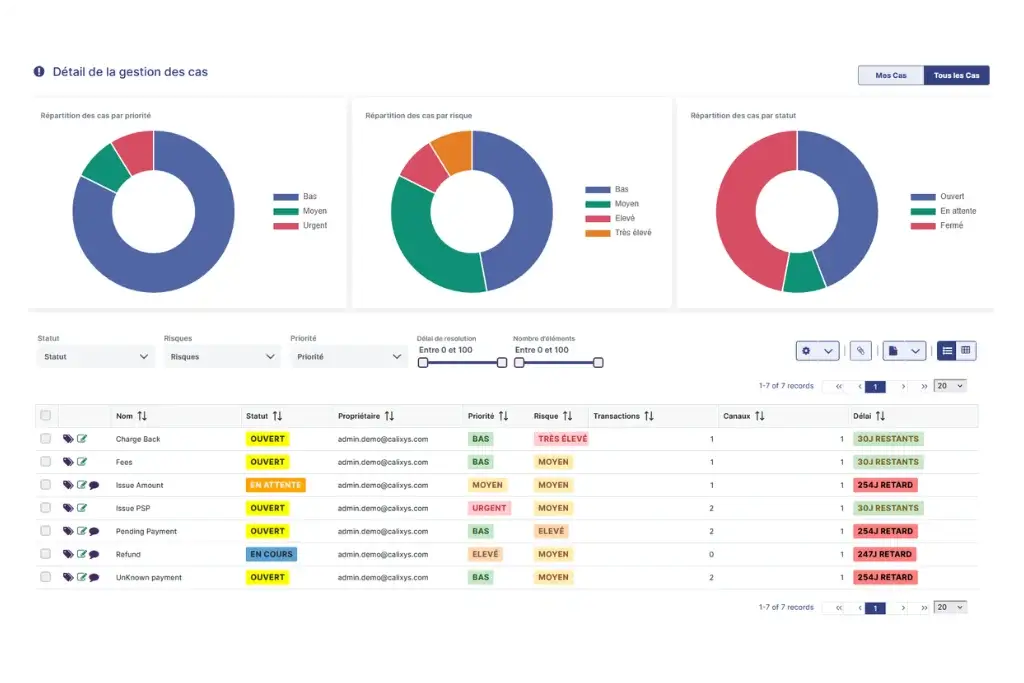

Any doubts? The CALIXYS Platform guarantees you a reliable accounting exercise

The CALIXYS Platform helps you complete your accounting exercise more quickly.

Indeed, it provides you with all the information you need. You can also automate all your data and perform bank reconciliations, which will avoid manual and repetitive tasks.

To avoid fraud and comply with regulations, our platform guarantees reliable and secure data. It facilitates control over your accounting entries and simplifies financial control operations.

You also have a 360° overview to check all transactions and accounting operations. CALIXYS is an easy-to-integrate platform and it adapts to your organization and your working habits.